Travel Demand Bulletin: Positive signs emerge for Europe’s hotel industry - Part 2

Forward-looking flight and hotel search data from OTA Insight’s free Global Market Insight tool paints an optimistic picture

After two years of pent up travel frustration, new flight and hotel search data indicate that consumers are planning to travel in the spring and summer of 2022. This, despite lingering uncertainty in Europe after Russia’s invasion of Ukraine, and the ongoing unpredictability surrounding Covid-19 travel restrictions.

Forward-looking flight and hotel search data from OTA Insight’s free Global Market Insight tool paints an optimistic picture, where we have seen an uptick in week-on-week demand for European destinations since the end of February, when the war in Ukraine started. As many as 3 in 4 Europeans are planning spring and summer vacations to destinations across Europe this year, and with high season fast approaching hotels across Europe have a chance to ensure they can maximise their bottom line, by targeting the right customer at the right time.

Pre-booking data from Market Insight gives insights into the demand evolution of any given destination, providing a window of opportunity for hoteliers to make informed commercial decisions, based on real-time forecast projections. By implementing an effective commercial strategy at this early stage in the booking cycle, hoteliers have a unique opportunity to turn lookers into bookers, ahead of their competition, and still ensure they are selling their inventory at the optimum price.

In Part 1 of this analysis, we looked at Amsterdam and Rome. In Part 2, we will examine flight and hotel search data for Barcelona, Berlin, London, Madrid and Paris.

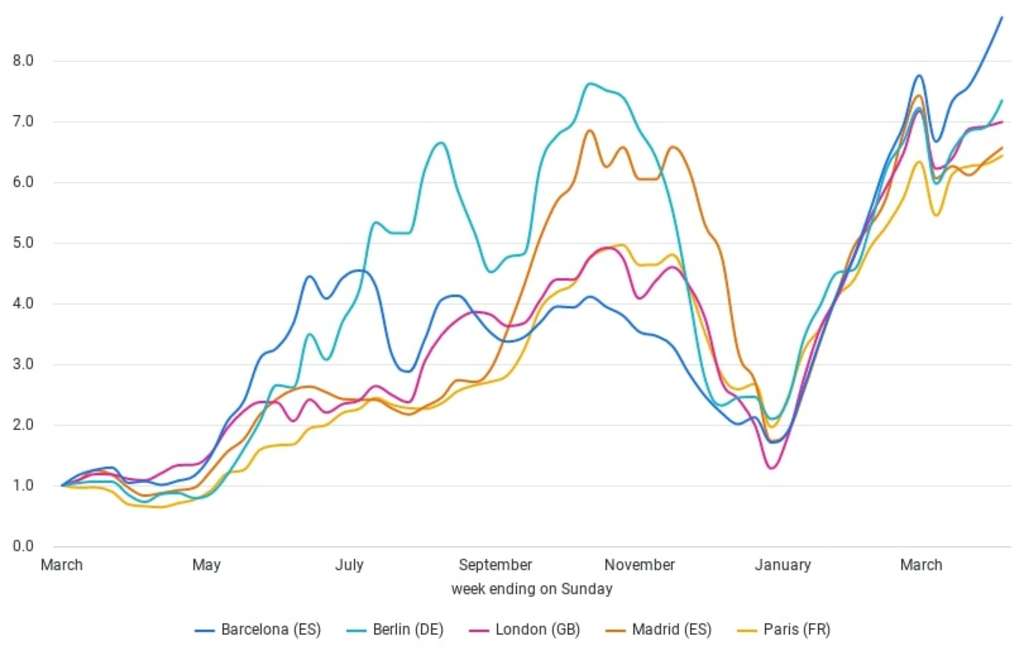

OTA and metasearch evolution Barcelona, Berlin, London, Madrid and Paris

Paris

In Paris, flight search queries in April 2022 are 12.85 times higher than they were at the same time last year. Following an upward trend in searches from January 2022, they dropped by 21% between the 21st of February and the 28th of February, when Russia invaded Ukraine. Search queries have since increased by 53% from what they were on the 28th of February. While hotel searches saw a similar slump at the end of February, they have seen a slower resurgence.

Despite this, they are still 9.7 times higher in April 2022 than they were at the same time in 2021, and GDS searches are 8.7 times higher than they were at the beginning of April 2021. In the last week 20% of hotel searches were from America, while 68% of flight searches were from within Europe, including the UK. After the relaxing of rules in parts of Asia, we are also seeing increasing flight searches from the Republic of Korea. In February just 5% of all flight searches were from Asia, but this has since risen to 16%..

There has been a clear shift in booking lead times, where consumers were either looking for quick getaways or dates well in advance. Search patterns show that 38% of hotel searches are for dates 29-90 days ahead, and 28% are for dates in the 8-28 day window - 10% more than at the beginning of March. In March 2021, 64% of searches were for dates more than 3 months away. Today, 27% of searches are for dates more than 90 days away.

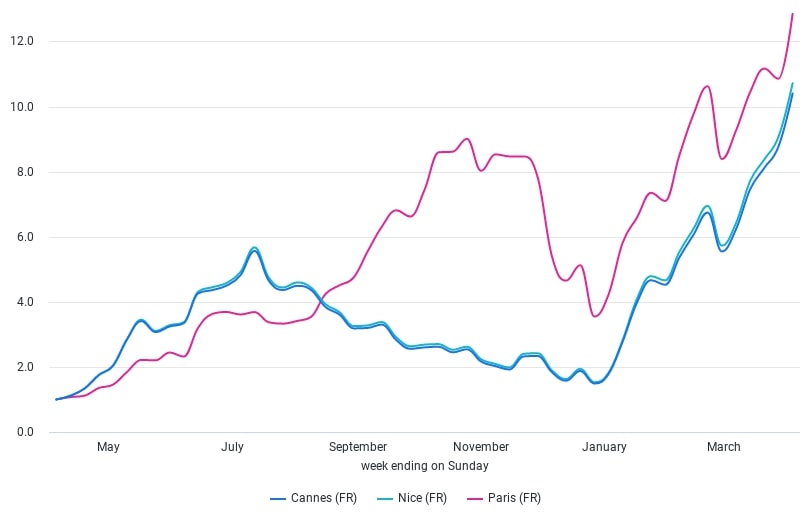

Other destinations in France, especially those along the southern coast, are also getting a lot of interest for the looming summer high season. Flight search data for Nice and Cannes show an 87% rise since the start of March, and 10 times more search interest than over the same period last year. In April 2021, just 8% of hotel searches were for dates in the 8-28 lead time window - 20% in April 2022. At the end of February, 16% of flight searches to Cannes were for dates in the 8-28 day window, but by the end of March, searches for dates within this window had surged to 28%.

Flight search evolution Paris, Nice and Cannes

London

The arrival of the Omicron variant in London at the end of 2021 saw a massive drop in hotel searches - to levels as low as they were in March 2021. But, with restrictions easing for both arrivals and departures to London, there has since been a steady uptick in searches for both flights and hotels.

In fact, there have been 5 times as many flight searches as there were at the beginning of January, and OTA searches have increased 4 times since then. GDS searches have also picked up considerably, and are 7 times higher than what they were in January. The pickup in hotel searches from January gathered momentum quickly. However, like other destinations around Europe, the uptick was disrupted due to the conflict in Ukraine, leading to an instant 19% drop in flight searches at the end of February.

Momentum resumed in the second week of March, and despite all travel restrictions falling away since then, the pick-up in hotel searches has not quite reached the same level as it had been before the war broke out.

OTA and metasearch evolution London

Search lead times have also shifted since March 2021. At that time, 73% of searches were for dates more than 90 days in the future. A year later, 31% of searches are for that same booking window. Currently, 37% of all hotel search traffic are for dates that fall in the in the 29 - 90 day window, up from 22% in 2021. While 10% of OTA searches were for dates in the 8-28 day window. And, while 10% of searches were for dates in the 8-28 day window in 2021, 24% of hotel searches are for dates within that booking window in April 2022.

Berlin

Berlin, too, has seen a large increase in both flight and hotel searches since March 2021 - 9.72 times as many flight searches, and 7.3 times as many hotel searches. Since January, this upward trend has continued and we have seen a 4.79 times jump in flight searches, and a 3.89 times rise in hotel searches, despite a disruption in the trend at the end of February.

Since January, searches also indicate a shift in the booking lead time windows to Berlin, where in the 8 - 28 day window, hotel searches went from 16% to 34%. In 2021, 11% of searches were for dates in the 8-28 day window, but this has increased to 34% a year later. 80% of Berlin’s flight search traffic is originating from within Europe, of which 15% are from the UK, 14% are from Spain, and 11% are from Italy. 85% of OTA and meta searches are also from within Europe, where 48% are from within Germany itself, and 10% of hotel searches are from the UK.

Madrid and Barcelona

In Madrid, both flight and hotel searches are 6 times higher than what they were in March 2021. 46% of hotel searches are from within Spain. 62% of all flight searches are from within Europe, and 32% are from the Americas. Of that, 11% are from Mexico, 10% from Italy, and 10% are from the UK. Just like comparable destinations, booking lead times are going back to more traditional patterns. 38% of hotel searches are for dates within the 8 - 28 day window, and 35% are searching for dates in the 29 - 90 day booking window.

There is a similar pattern occurring In Barcelona, though flight searches to Barcelona are 11 times greater than what they were in March 2021. Hotel searches, too, are 8.7 times higher than they were at the same time last year. And, while there was a slight dip in searches at the end of Feb, by the 2nd week of March, hotel search volume had started to climb again. GDS searches have also seen quite a dramatic rise since the beginning of 2022, and are 5 times what they were at the end of March last year. 89% of the flight search traffic is coming from within Europe, of which 21% is from the UK, 13% from Italy, 12% from Germany.

Summary

There are clear indications that demand is on the rise for some of Europe’s major cities. Much of the search traffic comes from other European countries, but as restrictions in other regions start to ease, there will likely be more interest from further afield.

While the war in Ukraine certainly affected consumers' immediate interest to travel, market intelligence data shows that this only lasted until the middle of March. It remains to be seen what the economic effects of the war will be on consumers, and how that could influence demand in the longer term. For now consumers are looking to break the shackles of two years of restricted travel.

With the help of forward looking data from Market Insight and Global Market Insight, we can see the travel demand forecast is looking positive for Europe, and that the booking lead times are returning to the more traditional 30 - 45 day sweet spot.

Armed with this data, hoteliers and their commercial teams can look to capture their fair share of the market by implementing a compelling pricing, marketing and distribution strategy, in the early stages of the booking journey.

In a highly dynamic market, it’s more vital than ever to have a competitive advantage over your compset.